You should be saving money and following good financial habits. Just don’t use a Savings Account to do it.

Savings accounts have long been listed as an essential part of a financial strategy, but that advice is outdated and, at this point, flat-out misleading. Even personal finance powerhouses like Bogleheads and You Need a Budget are coming around to the idea that savings accounts are not essential. Here’s a breakdown of why a savings account is unnecessary today.

Savings accounts do not build wealth

The top reason to keep your money in a savings account is that it supposedly earns interest.

This reason has been gone since the 2008 financial crisis. As recently as 2006, savings accounts paid 4% annual interest rates. In the 1980s, interest rates reached 20%.

As of August 2021, most savings account rates are virtually 0%. It has been 13 years and interest rates have never come close to pre-financial-crisis levels. Many experts think there is no reason to expect interest rates to rise again in our lifetime for a variety of reasons (Fed mandate to control inflation, technology advances, and access to capital are just a few I hear about in my day job).

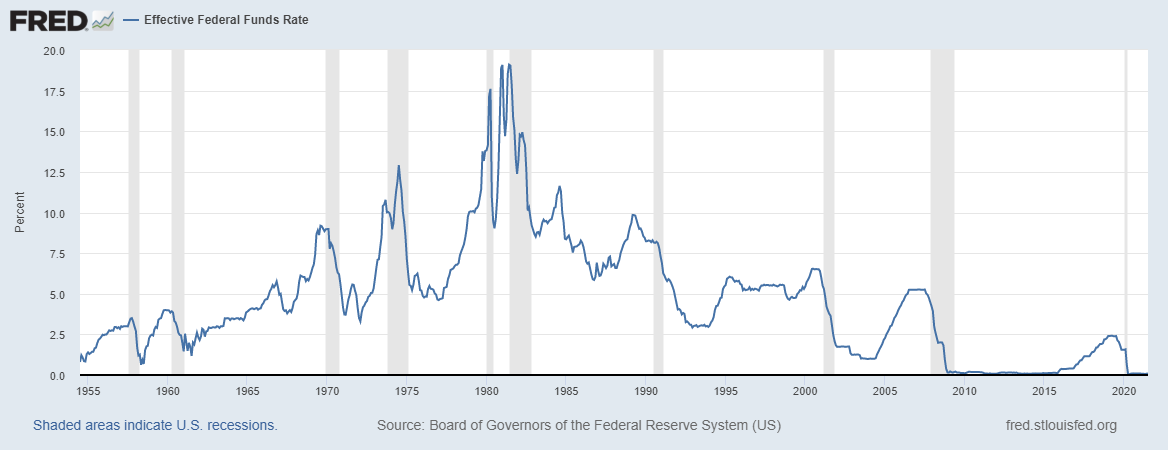

This graph of the Federal Funds Rate (upon which most savings account interest rates are based) below shows how interest rates have changed over the past 67 years. Notice how the line virtually disappears in 2008. Most of the time since then, interest rates have been effectively zero. It may look like the graph ends in 2020, but it doesn’t. Rates are just so low from March 2020 through August 2021 – even lower than the prior decade – that you cannot even see it.

The average savings account interest rate in August 2021 is 0.06% (August 2021 – NerdWallet). Take note of how minuscule that number is compared to what we just reviewed. It is effectively zero.

For comparison purposes, the 12-month inflation rate is currently 5.4% (August 2021 – US Inflation Calculator). That number is slightly inflated (pun intended) due to COVID, but the long-term inflation rate and Fed’s target is 2% (much higher than 0.06%). The highest yielding savings accounts right now are paying 0.55% (August 2021), still not even close. That means you are losing real money.

Many people don’t know what their savings account is paying; they just use their current bank’s savings account in tandem with their checking. Chase is the largest consumer bank in the U.S., and their savings account is currently paying a deplorable 0.01%. That means if you invested 10,000 dollars today, you’d have 10,001 dollars a year from now. To reiterate, you’d earn 1 dollar on 10,000. (And don’t forget, that 10,001 dollars would actually be worth less than 9,500 due to inflation at August 2021’s rate.)

Most people are smart enough to know they won’t get rich putting money in a savings account, and yet still list “earn interest” as a benefit to having one. It is not. You earn virtually nothing and have for the past 13 years.

Disclaimer: Interest rates in August 2021 are historically low, but they’ve been “historically low” for the past 13 years, so I am quoting them here to make my point. If you read this article in the future, these rates may change significantly. I can only vouch for their accuracy as of the time of this writing (August 2021).

Savings accounts will not fix your money habits

The second-largest reason cited to have a savings account is really a combination of reasons, all of which revolve around money psychology. These reasons range from “if you don’t see it, you won’t spend it” to “set aside money for something big” to “get a nice surprise!”

I am a big proponent of automating your finances, but this is much different than putting your head in the sand to avoid dealing with money. If you automate properly, you will achieve your goals and never worry about your money. You can do this without a savings account.

“If you don’t see it, you won’t spend it.”

If you feel an urge to spend every penny in your checking account, your relationship with money is flawed. Opening more accounts will not fix this. Figure out what you really need and spend on it without guilt, but cut mercilessly on the things you do not.

“Set aside money for something big.”

Planning ahead is great, but you do not require more accounts to do so. You can set a goal on a variety of websites (e.g., Mint) or simply track it on your own. Furthermore, how far away is this big thing? If it’s a few years away or an undetermined time, you’re probably better off investing. If it’s short-term, there is no reason you can’t keep it in your checking account.

“Get a nice surprise.”

First of all, don’t be so oblivious to your finances that you forget you have a savings account. Secondly, it will not be a surprise, because savings accounts do not build wealth, as noted above. If you put in $100/month for 24 months, you know what you’ll have at the end: about $2,400. You’d have the same amount if you put it under your mattress. While it is a good idea to develop a habit of saving like this, you’re better off investing that money rather than keeping it in a savings account (or under your mattress).

Savings accounts are worse than checking accounts

We’ve established that savings accounts do not earn meaningful interest and that using one will not fix your money habits. But, how do savings accounts compare to other options for your money?

Checking accounts are better than savings accounts. Checking accounts pay comparable interest (virtually zero) and give you full access to your money at any time. Savings accounts, on the other hand, only allow six withdrawals per month (subject to some exceptions).

Banks love to sell you on opening a savings account because they make more money on them than from checking. Due to lower reserve requirements, banks can loan out more from savings accounts because they are “non-transactional” accounts. (I don’t know about you, but most people don’t go out of their way to make their bank more money.)

Most checking accounts offer quality of life benefits, such as automated bill pay, debit cards, and ATM fee reimbursements. Many savings accounts have added similar benefits, but these are still heavily restricted. Since banks aren’t compensating you for these restrictions (again, they stopped paying meaningful interest 13 years ago), there is no reason you should impose them on yourself.

Checking accounts charge overdraft fees if you accidentally spend more than your balance. Having a decent cushion of money in your checking account eliminates this risk. Transferring this cushion to your savings account reintroduces overdraft risk for no reason. Sometimes, if both accounts are at the same bank, they’ll link the accounts so that your savings account is a backup. However, this is an unreliable and unnecessary complication that could leave you stuck with a terrible savings account, like Chase’s.

For what it’s worth, my checking account at Schwab is currently paying 0.03% (August 2021) interest, which is still nothing, but more than Chase’s savings account at 0.01%. I get all the flexibility of a checking account and none of the restrictions of a savings account. I simply keep my checking balance high enough so I can pay several months of bills, if necessary.

Savings accounts are worse than investment accounts

In addition to checking, another place you can put your savings is investment (or brokerage) accounts.

Investment accounts are better than savings accounts. You shouldn’t invest money you can’t afford to lose, but as determined above, there’s no reason you can’t keep that short-term money in your checking account. What should you do with the rest?

If you aren’t investing you are losing money. The long-term average inflation rate, and target for the Fed, is 2% per year. You need to earn that much just to maintain your money’s purchasing power.

Both tax-advantaged (e.g., retirement) and taxable brokerage accounts open up a world of stocks, bonds, mutual funds, and ETFs. Diversify and invest responsibly, and you can earn a reasonable return with limited downside. This is how you grow wealth. Savings accounts do not do this; they erode wealth.

General brokerage accounts (non-retirement) generally give you complete access to your money as well. You’ll own “liquid” investments, meaning you can easily sell them and use the money the next day. The account will be linked to your checking account to allow instant transfers, the same way your savings account would.

If you really want the money out of your checking account but do not want to invest right now, you can leave some cash in your brokerage account. Personal brokerage accounts are notorious for not paying interest on your cash, but neither do savings accounts. It is a fine temporary place to store money.

Savings accounts are not “emergency funds”

“Emergency Fund” is a silly term that means “keep some safe and liquid money around for unexpected expenses.” The term “emergency” complicates what is a simple financial practice. The recommended amount is 3 to 6 months of expenses (the logic being that the most common “emergency” is losing your job, and it takes that long to find a new one).

While most people should indeed keep (at least) a decent cushion of 3 to 6 months of expenses, this can be kept in your checking account as discussed above. You don’t need a separate account for this.

Some of it can also be kept in your brokerage account, either as cash or in low-risk, liquid investments. The larger the cushion of money in your brokerage accounts, the less you need to worry about having a specific amount for an “emergency” and the more risk you can take (and therefore more wealth you can build).

Is there any reason at all to have a Savings Account?

I constantly underestimate the psychological barriers that people face with money. It boggles my mind that anyone can find themselves in credit card debt, yet nearly 40% of Americans do. I cannot comprehend why anyone would not be able to control their spending simply because they “see” more money in their checking account, but many people face this challenge. If anything, I strive to do the opposite, because having more in your checking account protects you from overdraft fees.

I do not believe a savings account is the cure for these ailments. If you do need to keep the money “out of sight,” there is no reason not to open a brokerage account instead. You do not even need to invest it right away, but at least you have the option to do so. It will not earn any interest there, but it would earn virtually no interest in your savings account anyway.

Personal finance gurus might be quick to jump down my throat for suggesting that no one should have a savings account. Perhaps my view is skewed as an investment professional, but shouldn’t everyone be striving to think like the pros?

TLDR: No one needs a savings account in August 2021, nor for the past 13 years. It is antiquated advice from an era that has been gone since 2008. It pays negligible interest and provides no actual benefit; however, it may provide some perceived benefit to those who are not psychologically sound with their money habits.

If you can think of a reason I haven’t thoroughly debunked, I’d love to hear about it.

Comment below, find me on twitter @mjdesimone, or email me your thoughts at mike@michaeljdesimone.com. I read every email.

P.S. Timing is everything. At the time of this writing (August 2021): as a result of this investigation, I cannot find any good reason anyone should have a savings account. I stress the phrase “at the time of this writing” because there was a time when interest rates were a compelling reason to have one. However, that time is long past. Whether or not it will come again is anyone’s guess, but many experts think not. Anything can happen though…this article may look ridiculous a few years from now. The question to ask is, “how high do interest rates need to get to be worth it?” That’s tough to answer because everything is relative, but I probably wouldn’t consider them again unless they reach pre-2008-crisis levels (around 4%).

LOCALIZATION: This was written primarily for US residents. Factors unique to other countries may not have been considered.

DISCLAIMER: This is education, not financial advice. All investment/financial opinions expressed are my own and not related to my employer or any other person or entity. They are based on personal research and experience and are intended as educational material.

I am not your financial advisor. I am not a registered investment, legal, or tax advisor or a broker/dealer. This content was not created for or catered to any individual person or group, so no one should treat it as personalized content. All content was accurate and up to date as of the publishing of the article to the best of my knowledge.

Do your own research. This content is provided for informational purposes only. It is important to do your own analysis before making any investment based on your own personal circumstances. You should seek the advice of a financial professional and independently verify any claims made before making any investment decision.

Investments may lose money. All investments involve risk and you should be sure you understand your exposure and tolerance for that risk before making an investment decision. Past performance is not a guarantee of future return, nor is it necessarily indicative of future performance. The value of your investments will fluctuate and you may gain or lose money.

One response to “Does Anyone Actually Need a Savings Account?”

Very informative! Thanks for the facts!